Commerce Development Research Institute released the Business Cycle Coincident Composite Index for Taiwan Service Sector today (5th Mar). The actual value has peaked since May last year and has been declining since December. The predicted value is lower than the long-term trend value (100) in February this year, which means that the economy is likely to be entering a recession. Although it may pick up in May and June, it will see a decline in July. It shows that the short-term recovery is painful, but it does not cause a rapid fall. However, the low-end stagnation indicates that necessary measures should be applied.

The system uses the leading indicator cycle index to predict the future trend of the coincident index.

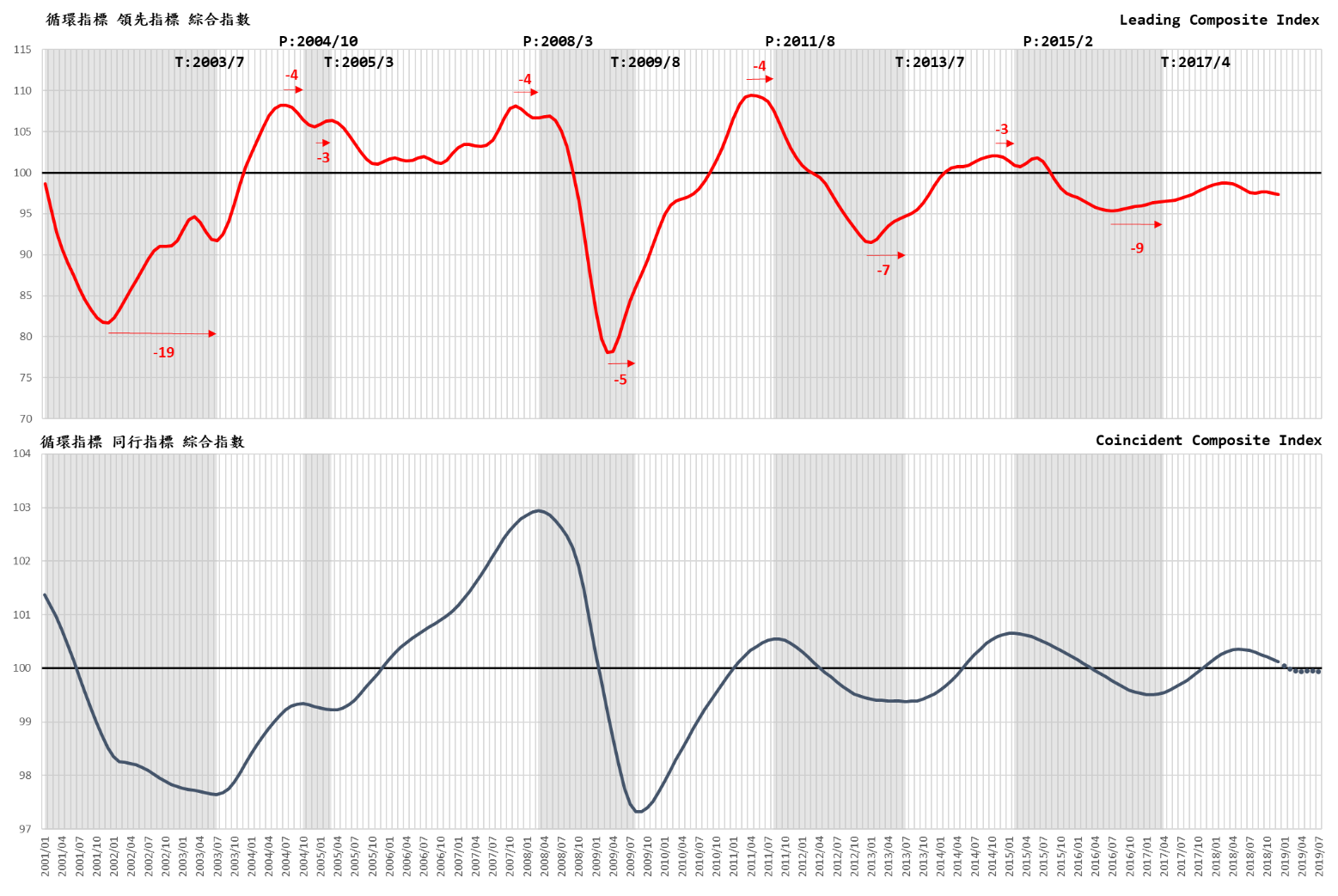

The actual value of the leading indicator cycle composite index hit the top in March last year. After five months of decline, it rebounded again in September and October but declined again in November and December. Therefore, the forecast of the coincident composite index representing the actual economic changes from last year. After hitting the top in May and then turning down for 11 months, it will fall again in July after the slight increase in May and June this year. According to this trend, the economy is still difficult to see a rebound in the short term, but it will not fall sharply. The predictive value coincident index comprehensive cycle index has started to fall below the long-term trend value (100) in February, indicating that the economy is entering a recession, and it is highly likely that an L-shaped recovery will be formed, indicating that there is a need for proactive redeem measures.

The actual value of the Cyclical Leading Composite Index for service industries (excluding long-term trend cycle values) peaked in March 2018 and then fell. Its cycle index has fallen from 98.76 in March to 97.53 in August and rebounded to 97.64 and 97.68 in September and October, but it has turned down again since November, to 97.34 in December. It is shown that the coincident indicators that predict GDP on this basis will continue to fluctuate again.

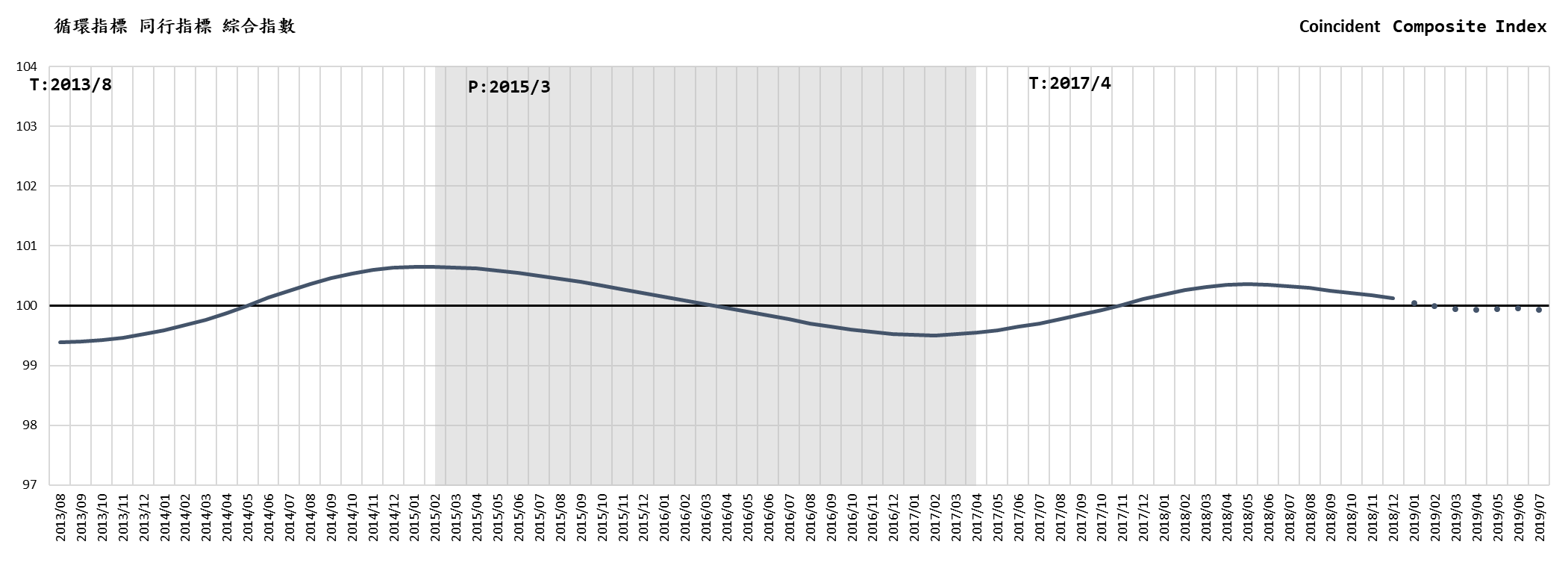

The coincident composite index, whose actual cycle value peaked at 100.36 in May 2018, then fell to 100.12 in December. The predicted value will start to fall below the long-term trend (100) in February 2019 and will fall to 99.94 in April this year. Although it will pick up in May and June, it will fall to 99.93 in July and return to the level of October 2017 (as shown below). This means that without positive and effective economic incentives, the overall service industry will continue to fluctuate downwards. Once the recession becomes a reality, it will not only indicate that the recovery since March 2017 last only 15 months, which is quite a short recovery, and the current slowdown will also be low, and it will be difficult to see a bright rebound in the short term. It is currently appropriate to continue to strengthen more proactive and effective incentives. First of all, in the case of different sub-indicators in different sectors, it is not appropriate to merely carry out the general, traditional public fiscal deficit or quantitative monetary easing measures but to improve the supply efficiency and promote effective efficiency in different departments. In particular, the current stage of economic development is facing an unprecedented world of "netizens" mobile, digital, intelligent, and the networked new industrial revolution. The domestic market is small, export-oriented in Taiwan, more necessary and feasible IT with the advantages of science and technology and the foundation of strong private capital, we will vigorously carry out the digitalisation of industrial structure and the transformation of new internationalisation. We should put the "second curve" of long-term economic development on the right track and restore the long-term trend of the high-growth new economy.

The recent trend of Coincident indicator cycle index

The recent trend of Coincident indicator cycle index

The trends of sub-indicators of coincident index vary in different sectors, the composite index has continued to decline in June 2018, and the rate of decline accelerated in Q4. It is predicted that the cycle index will be lower than the long-term trend (100) in February this year, and then wave moving downwards, it will fall to 99.93 in July, indicating that the current slowdown is hard to see and because the cycle index will be below 100 for the long-term trend, it shows that the economy is in danger of falling into recession.

The sub-indicators of the coincident index (which can suggest the real GDP changes in the service industry), however, see different trends in different sectors.

|

|

Year/Month

|

Cycle Index

(Trend value=100)

|

Remark

|

|

2019-07

|

99.9345

|

(p)

|

(P): Predicted by leading indicator from Jan 2019 to Feb 2019

|

|

2019-06

|

99.9560

|

(p)

|

|

2019-05

|

99.9505

|

(f)

|

Forecast based on the actual value of the Composite Index of Leading Indicators

|

|

2019-04

|

99.9358

|

(f)

|

|

2019-03

|

99.9463

|

(f)

|

|

2019-02

|

99.9909

|

(f)

|

|

2019-01

|

100.0455

|

(f)

|

|

2018-12

|

100.1243

|

(a)

|

The actual value of the Cycle Coincident Composite Index

|

|

2018-11

|

100.1703

|

(a)

|

|

Source: Business Cycle Forecasting Team, CDRI

|

(a) actual

(f) forecasted

(p) predicted

|

|

Business Cycle Coincident Composite Index for Taiwan Service Sector Business Cycle Composite Index for Taiwan Service Sector

Business Cycle Composite Index for Taiwan Service Sector

Source: Business Cycle Forecasting Team, CDRI

Previous cycle:

|

Cycle

|

Trough

|

Peak

|

Trough

|

|

1

|

2003/7

|

2004/10

|

2005/3

|

|

2

|

2005/3

|

2008/3

|

2009/8

|

|

3

|

2009/8

|

2011/8

|

2013/7

|

|

4

|

2013/7

|

2015/2

|

2017/4

|

(Business Cycle Indicator System is designed, instructed and analysed by professor Tain-Tsair Hsu)