The slowing down growth of Taiwan’s service industry is expected to continue, but at a slower pace, until February 2020.

The high tide of manufacturing back home has highlighted a stunning hope to upturn the Taiwan’s 3-decade low investment and economic growth.

Nonetheless, in the face of the current global economic and geopolitical turmoils as well as the slow growths in domestic employment, consumption, financial sector, and demand divergence among industries, the CDRI recommends that the government is better to adopt “precision policies” while implementing stimulus measures.

The Commerce Development Research Institute (CDRI) releases the Business Cycle Coincident Composite Index for Taiwan Service Industry today (4th October). It is predicted that the economic slowdown will continue until February next year. Despite the divergence among industries in terms of economic outlooks, the aggregated demand will persist to decline albeit at a slower pace.

Among the sub-indicators of all leading indicators, the “Private Real Fixed Capital Formation” continues moving upwards, the “Trade Deficit in the Service Industry” remains shrunk; nonetheless, “Real GDP of Transportation & Warehousing”, “Net Rate of Employment Increment in the Service Industry” and “Case of First-time Unemployment Benefit Claims” have all worsened continuously.

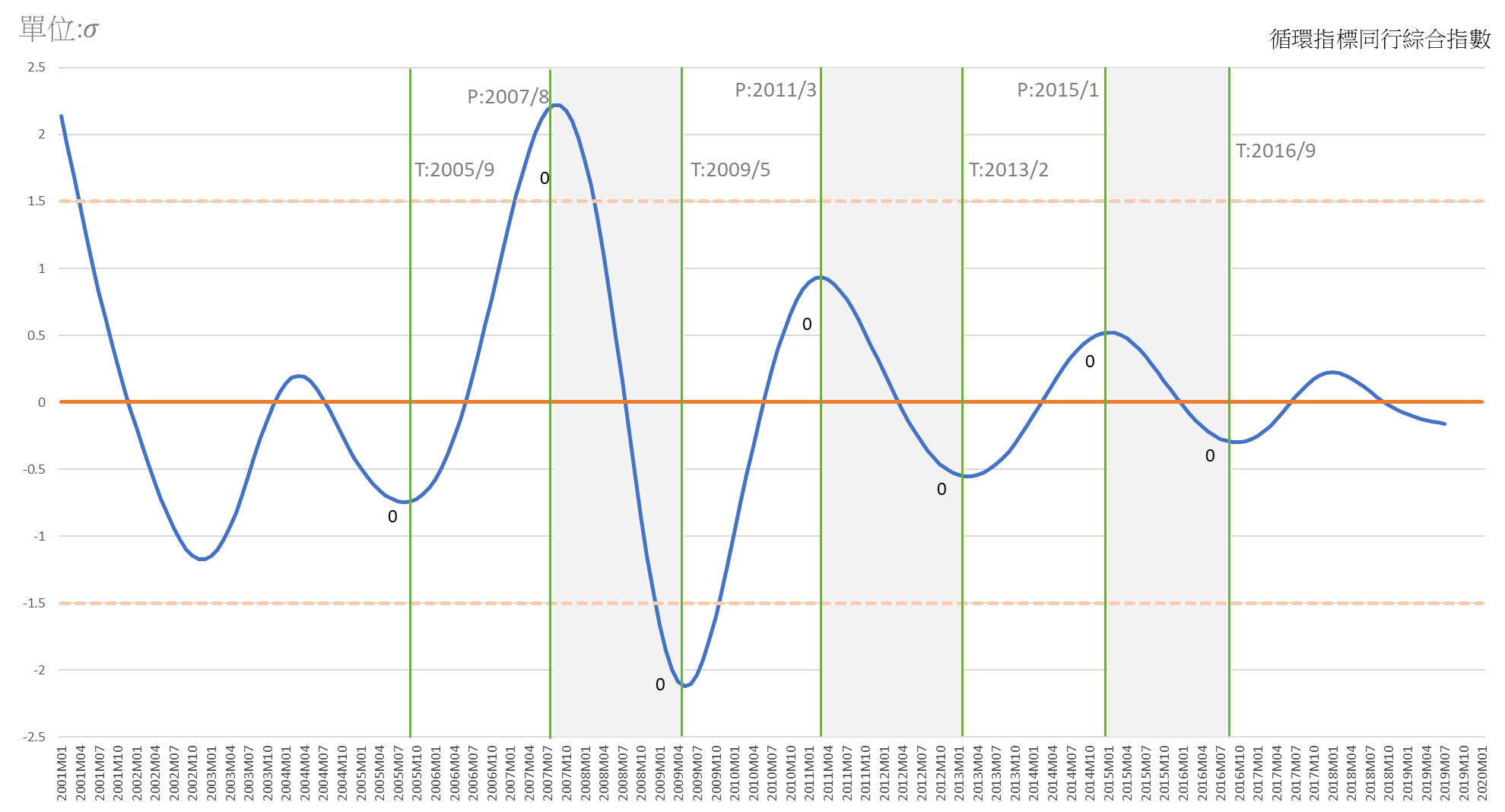

The Business Cycle Coincident Composite Index began to fall since the beginning of 2018, and then fell faster in the second half of 2018, and peaked in the first half of 2019. It is forecasted that the index will continue falling at a slower rate from September 2019 to February 2020.

Meanwhile, the sub-indicators of the cyclical coincidental composite index move in different directions. Both of “Wholesale & Retail Sector and Finance & Insurance Sector” have decreased modestly whereas the “Real Estate Sector and Residential Services Sector” keeps moderately increasing. And, the number of people employed in the service sector has decreased a bit. Its cyclical index was a bit below 100 ( the long-term trend).

Under these circumstances, we speculate that the traditional means of fiscal and financial policies would not work again like before, therefore suggest that a kind of new stimulus measures of “precision policies” in accordance with the situation of each sector is worth of undertaking.

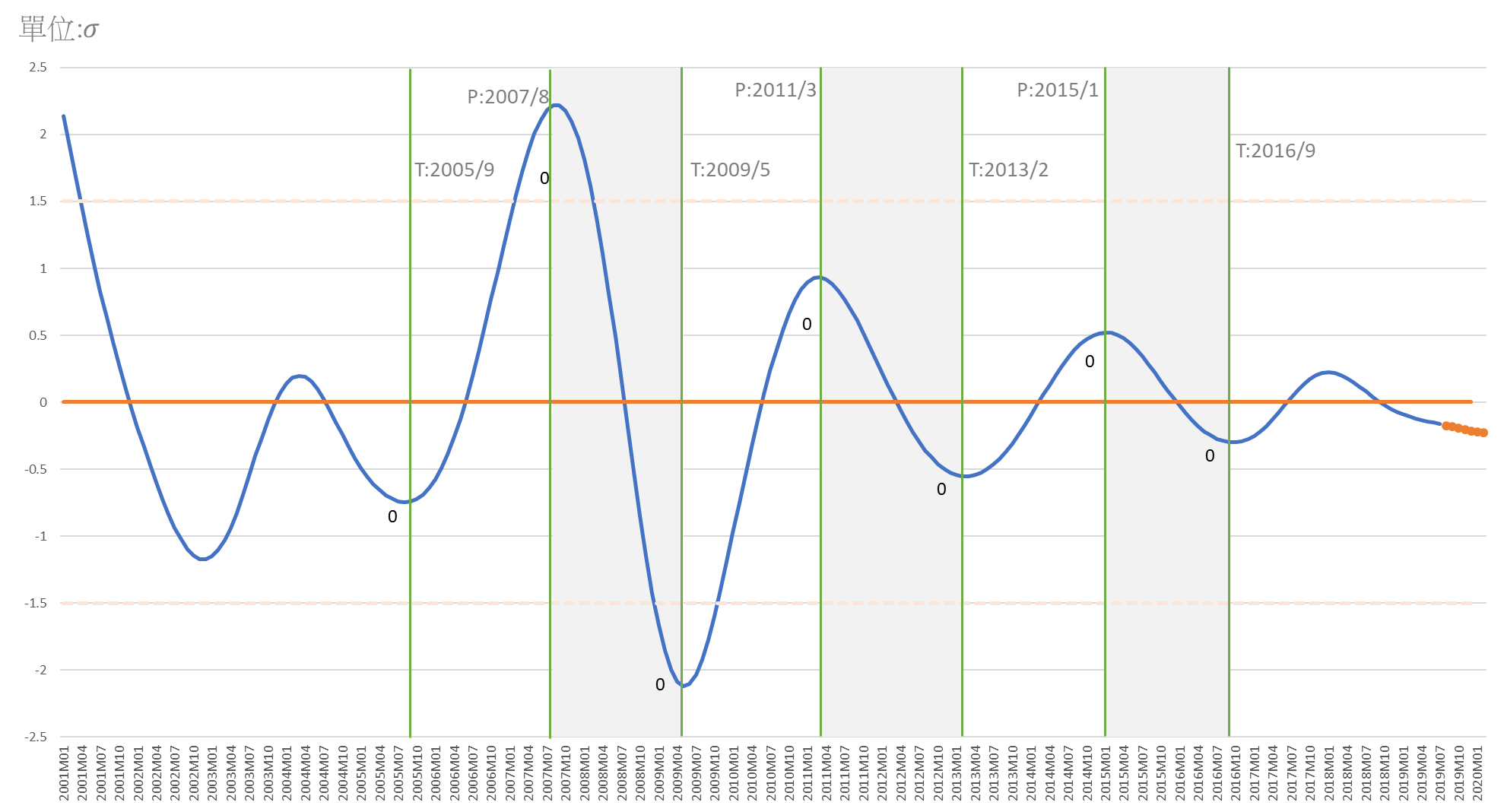

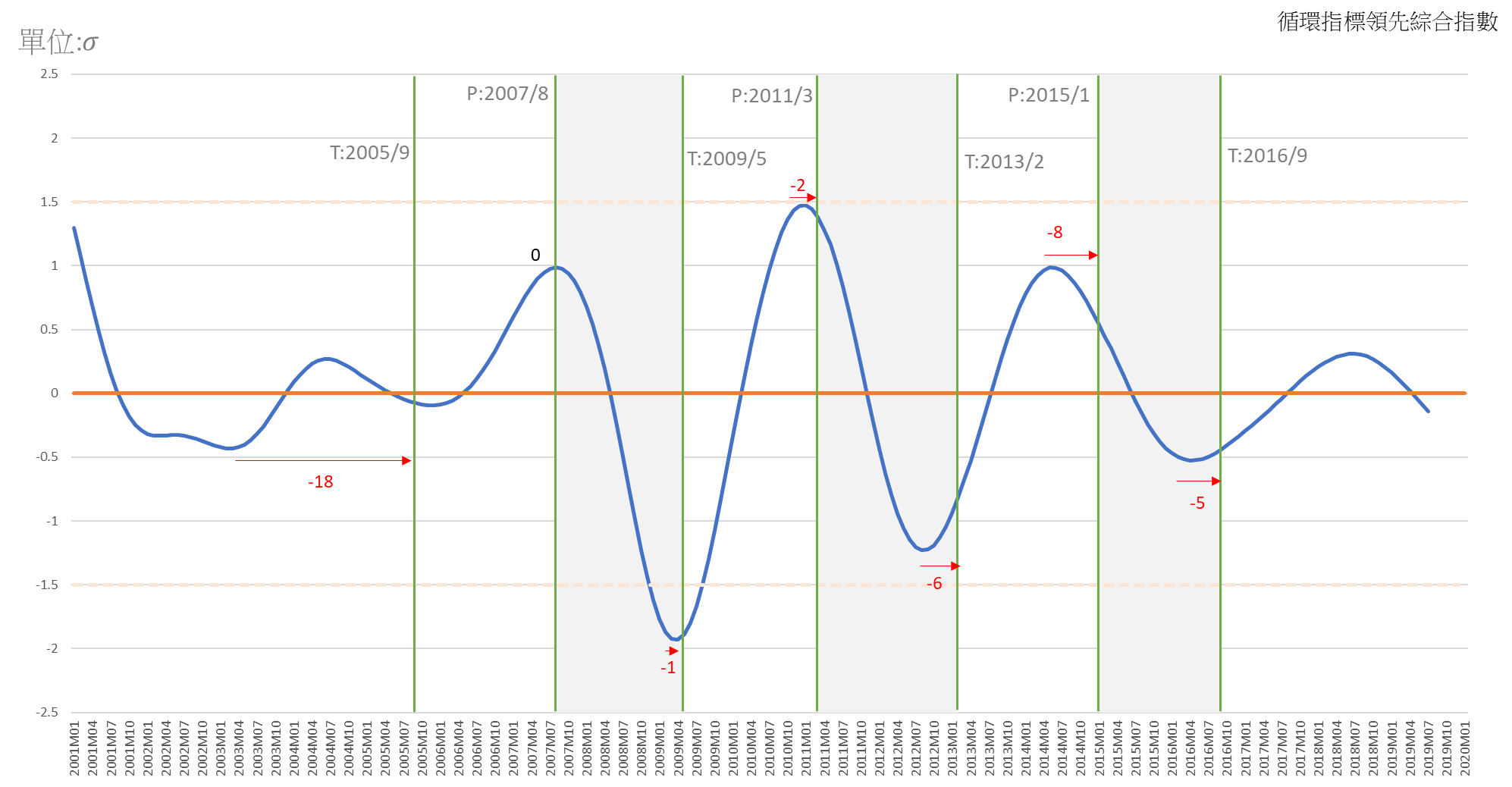

The Fluctuations and Forecasts of Cyclical Coincident Composite Index

Note: Shaded area represents slowdown or recession in the service growth as determined from trend-adjusted measures of aggregate sale and employment. The dates are recognized as the reference cycles.

Explanation: According to the past indication, upward indicates a rise in the economy (recovery), downward indicates a decline (slow or recession), between zero and 1.5 σ indicates recovery, above 1.5 σ indicates prosperity; between zero and negative 1.5 σ indicates sluggishness or decline, and less than 1.5 σ indicates depression.

Business Cycle Coincident Composite Index for Taiwan Service Industry

|

Year/Month

|

Deviation of Standardized Cycle Indicators

(Unit: σ, Benchmark: 0)

|

Remark

|

|

2020-02

|

-0.2299

|

(p)

|

Prediction based on the lead effect for six months of the ARMA Model:(4,0) (0,0)

|

|

2020-01

|

-0.2214

|

(p)

|

|

2019-12

|

-0.2162

|

(p)

|

|

2019-11

|

-0.2068

|

(p)

|

|

2019-10

|

-0.1965

|

(p)

|

|

2019-09

|

-0.1858

|

(p)

|

|

2019-08

2019-07

|

-0.1743

-0.16

|

(e)(e)

|

The estimated value of the coincident composite index

|

|

2019-06

|

-0.1530

|

(a)

|

The actual value of the coincident composite index

|

|

2019-05

|

-0.1425

|

(a)

|

|

Source:Business Cycle Forecasting Team, CDRI

|

| |

|

a

|

(actual)

|

|

|

|

e

|

(estimated)

|

|

|

|

p

|

(predicted)

|

Business Cycle Composite Index for Taiwan Service Industry

Chart 1. Cyclical Leading Composite Index

Chart 2. Cyclical Coincident Composite Index

Source: Business Cycle Forecasting Team, CDRI

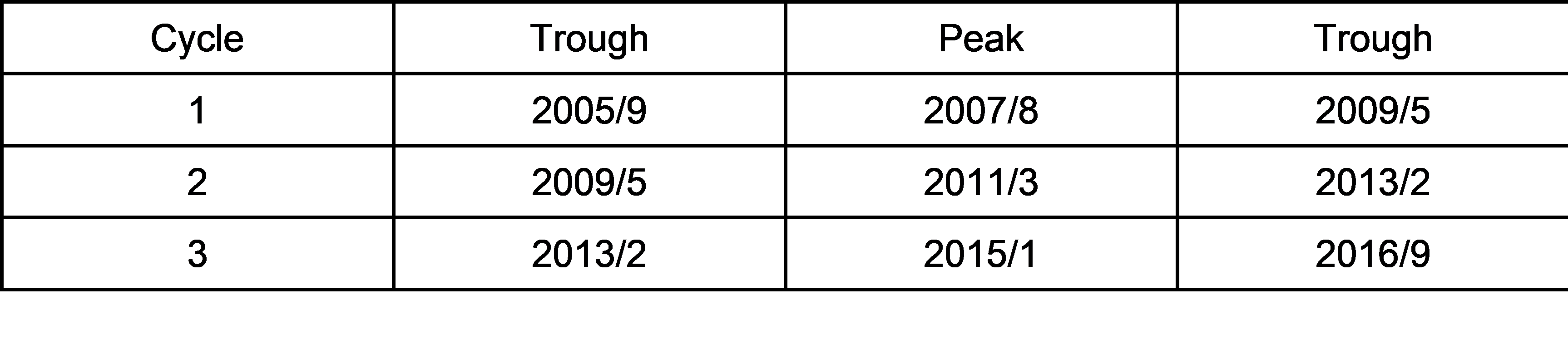

Table: The Reference Cycle of Taiwan’s Service Industry (Business Cycle Indicator System is designed, instructed and analyzed by Professor Tain-Tsair Hsu)