We are experiencing the longest record and the strongest effect of the Taiwanese manufacturers returning investment in 20 years which has spread to financial activities and has gradually affected the net entry rate of employees in the business service industry. It is predicted that the “Coincident Composite Index” of the Business Industry Cycle Indicator will end the 15-month decline in June this year. This means that we can be optimistic about the trend of the economy in the second half of the year. Over the past 20 years, China has been driven Asia’s powerful economic growth, yet its suffering from its internal structural imbalances and the crisis of the US-China trade war, and the unpredictable spread of "Wuhan Pneumonia". In particular, the Asian economy has suddenly been filled with uncertainty.

The magnitude of the impact of the epidemic will depend on the length of time it affects the mobility and liquidity of economic activity, such as the breadth and amplitude of the spread. Examining Taiwan's current economic capital and technological potential, especially the opportunity given to Taiwan's industrial structural transformation and new international development during the take-off of the global digital economy, Taiwan's economy in 2020 still has own chance to turnaround.

The SARS which broke out in 2003 is much different from the Wuhan Coronavirus epidemic in 2020, the neo-liberal FDI (Foreign direct investment) in Taiwan in 2003 the globalized world economy continued to move up to its peak. However, Taiwan’s economy continued to go slow back then. In 2020, the world's FDI will decline, and the main economic momentum replaced by it will be the investment and development of countries in the "digital economy." Taiwan has a chance to rise again. Asia's economic growth will still rule the world, but its protagonist is no longer China, but a peripheral connection in the era of edge computing. Taiwan can be one of the hubs. In the short term, although the impact of Wuhan Coronavirusa on Asian countries is unavoidable, it may accelerate the backflow of Taiwanese businessmen and the order transferring.

Commerce Development Research Institute(CDRI)released the Business Cycle Coincident Composite Index for Taiwan Service Industry today (5th February), the declining is expected to stop by June this year. Although there are still many indicators that continue to decline, the rate of decline has continued to slow down. Conversely, the continued increase in physical investment and financial output, have led to a slight rebound in the net entry rate of leading business service employees, making this year ’s optimistic expectations expected to continue to become more apparent (see attached figure 1 and text below). Yet the sudden outbreak of "Wuhan Coronavirus" (China announced the seal - off of Wuhan City from 10 am on 23rd January ") will threaten the world economy. Even if the stagnant can pick up as soon as possible, it will have to wait for the overall effective demand or the development of new consumer power in new markets. Now it is even more necessary to accelerate the development of the "digital economy" to make up for the loss of the "mobility" of the traditional economy from the impact of Wuhan coronavirus and to increase the "liquidity" through new digital economic investment.

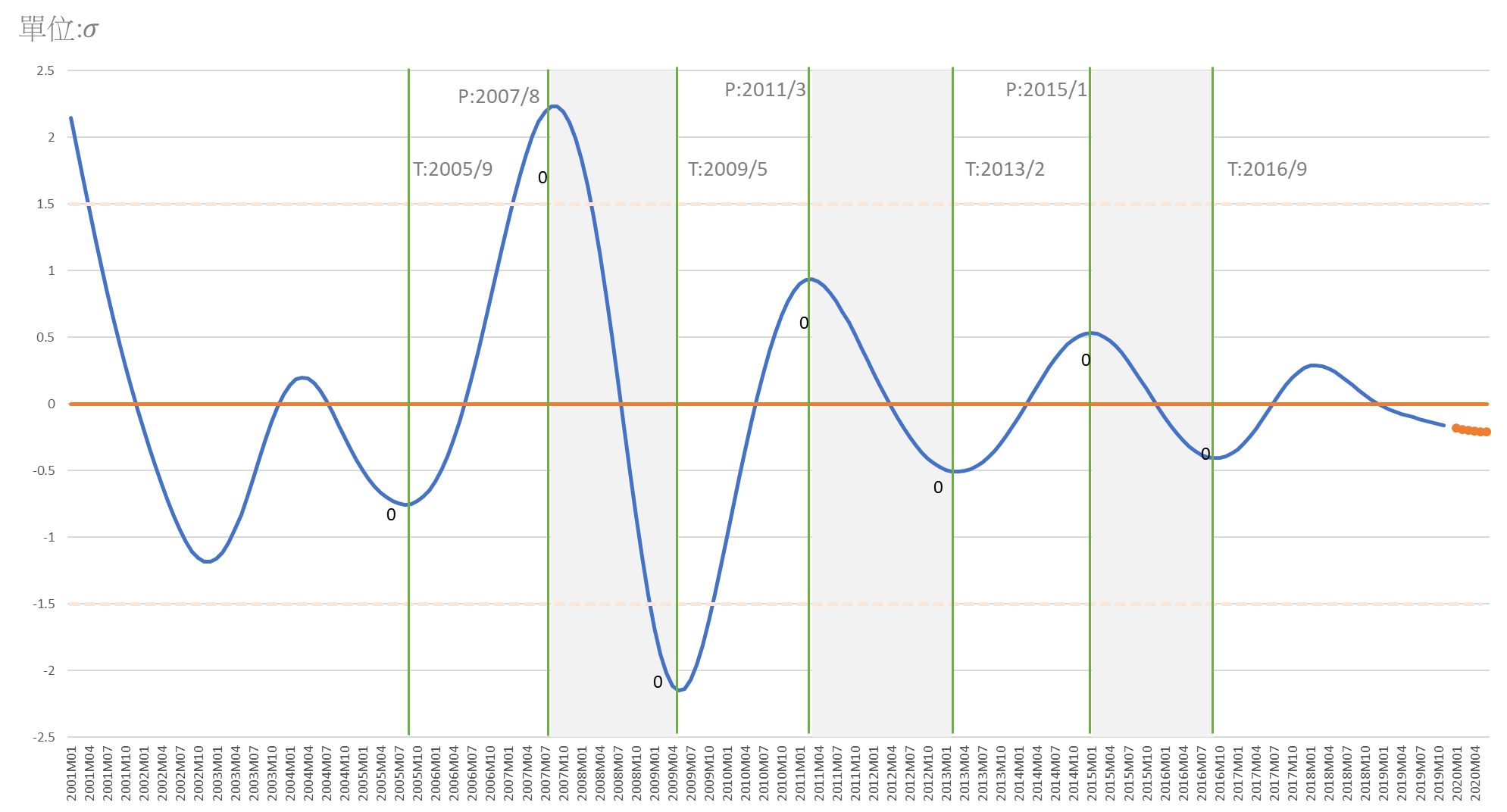

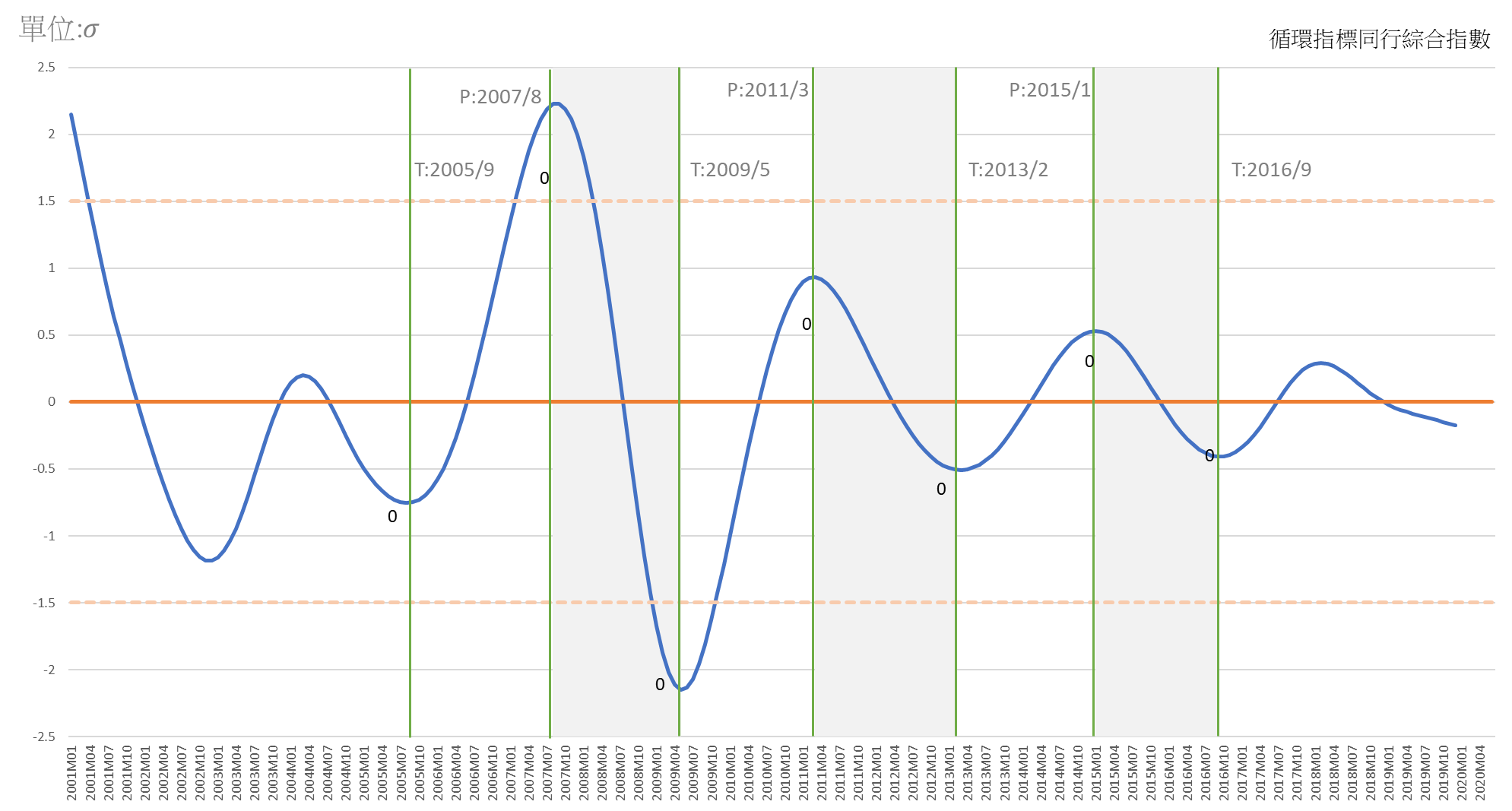

The following chart 1 shows the forecast for the business cycle index system. Until June, the decline of the Cyclical Coincidental Composite Index for Service Industries, which represents the business trend of the service industry, has been stopped slowing down and is expected to rise. This is the first time that the circular trend has stopped for 17 consecutive months since it began to fall below the long-term trend level in January 2019.

Chart 1 Trend and Forecast of the Business Cycle Coincident Composite Index

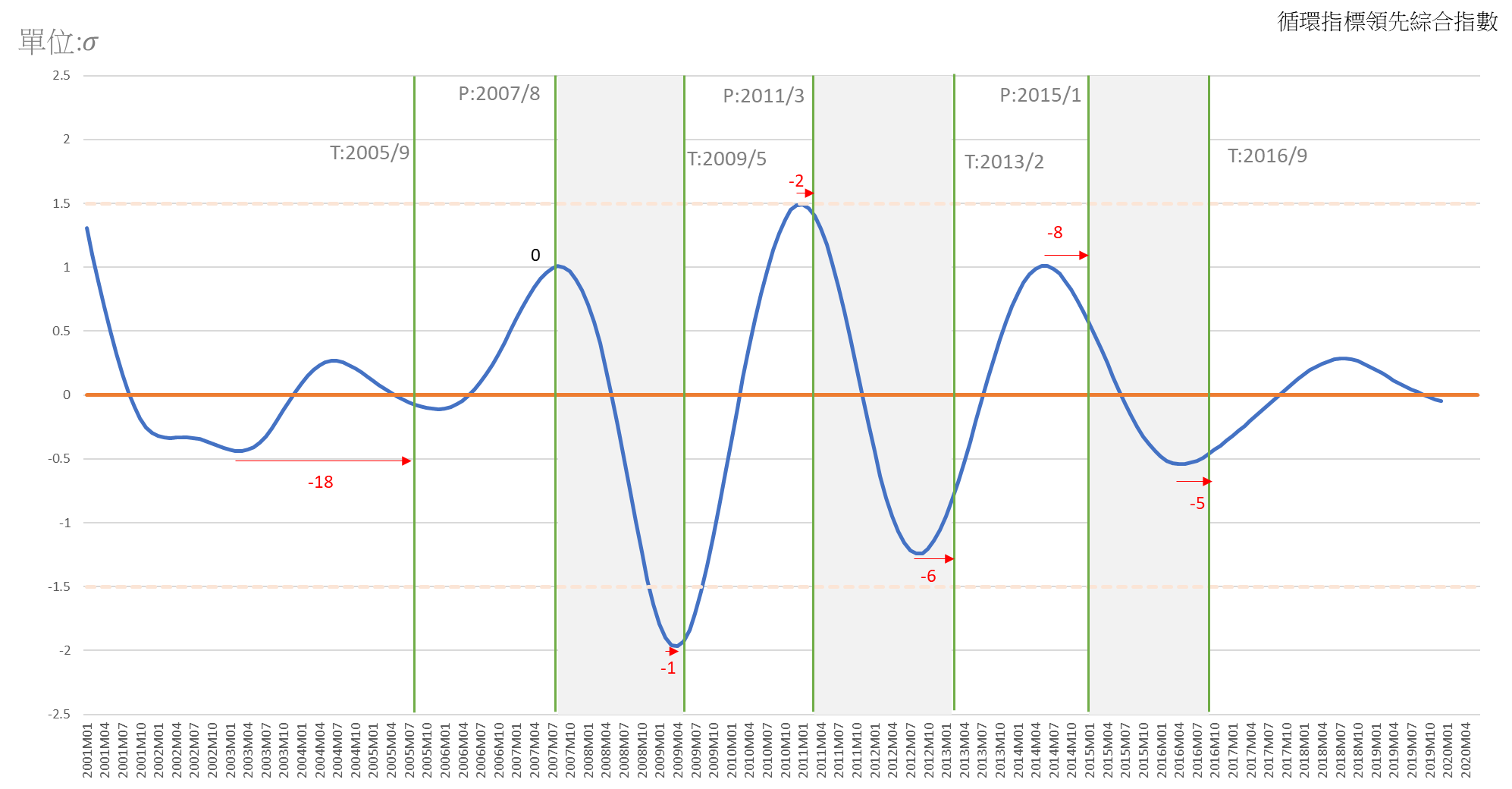

A. The actual value of the Cyclical Leading Composite Index for Service Industries(Long-term trend excluses) peaked in August 2018 and then continued to decline until December 2019. Its slowdown began to decelerate in May 2019 until now. The reason is that since the " Private Real Fixed Capital Formation" began to stop falling and rose in March 2018, the business cycle index has continued to climb, and began to exceed the long-term trend value (100) in January 2019, reaching 103.09 in November. The long-term deficit of the service trade has also been shrinking since January 2017. The circular trend value began to exceed the long-term trend (100) in August 2018 and reached 100.97 in December last year. The net employment entry rate of commercial service business has also seen a continuous increase in the long-term trend value (100) for seven months. Although other sub-indicators, including transportation and warehousing, employment and the stock market, continued to decline, the decline continued to decelerate. As a result, the decline rate of the overall service industry's business cycle leading composite index has slowed down significantly.

B. The overall commercial service industry business forecast is expected to stop declining by June 2020 and hopefully will rise soon。

Among the coincident indicators of various business cycles, in addition to the "real GDP of the financial and insurance industry", which has been declining since May last year, and has continued to increase slowly, the remaining "real GDP of the wholesale and retail industry" "employees and workers", "real GDP of real estate and residential services" and "real consumption of residential services, utilities, gas and other fuels" all continued to decline slowly.

The Deviation of Standardized Composite indicators is represented as the Units of Standard Deviation. From the peak (0.29 standard deviations (σ)) of February 2018 to February 2019, it decreased to - 0.02 standard deviations (σ) in January 2019, and then -0.14 deviation in September 2019.

It is predicted that in June this year, it will maintain the same level of -0.2 standard deviations as in May. It is expected that the downward trend will stop. However, in order to strive for a prosperous economic recovery as soon as possible, anti-aging or incentive measures can still be strengthened. It is generally acknowledged that investment in new digital technologies and the use of business models are the main drivers of economic growth.

Business Cycle Coincident Composite Index for Taiwan Service Sector

|

Year/Month

|

Cycle Indicators

(Unit: σ, Benchmark: 0)

|

Remark

|

|

2020-06

|

-0.2090

|

(P)

|

Prediction based on the lead effect for six months of the ARMA Model:(4,0) (0,0)

|

|

2020-05

|

-0.2090

|

(P)

|

|

2020-04

|

-0.2059

|

(P)

|

|

2020-03

|

-0.2002

|

(P)

|

|

2020-02

|

-0.1923

|

(P)

|

|

2020-01

|

-0.1828

|

(P)

|

|

2019-12

|

-0.1721

|

(f)

|

The estimated value of the coincident composite index

|

|

2019-11

|

-0.1607

|

(f)

|

|

2019-10

|

-0.1488

|

(f)

|

|

2019-09

|

-0.1367

|

(a)

|

The actual value of the coincident composite index

|

|

Source: Business Cycle Forecasting Team, CDRI

|

|

Note:

|

|

a

|

(actual)

|

|

|

|

f

|

(estimated)

|

|

|

|

p

|

(predicted)

|

Business Cycle Composite Index for Taiwan Service Sector

Source: Business Cycle Forecasting Team, CDRI

Previous Cycles:

|

Cycle

|

Trough

|

Peak

|

Trough

|

|

1

|

2005/9

|

2007/8

|

2009/5

|

|

2

|

2009/5

|

2011/3

|

2013/2

|

|

3

|

2013/2

|

2015/1

|

2016/9

|