Noted: The possible effect of the COVID-19 epidemic hasn’t been concluded in the system. COVID-19 is continuing to spread; short-term impact is inevitable in the future. However, the geological factors of the epidemic are expected to strengthen the return of Taiwan business people and transfer purchase orders caused by the trade and technology war. The virtual market can play a considerable substitute role in the short term. The government ’s outstanding epidemic prevention capabilities and active efforts on financial relief will boost the economy.

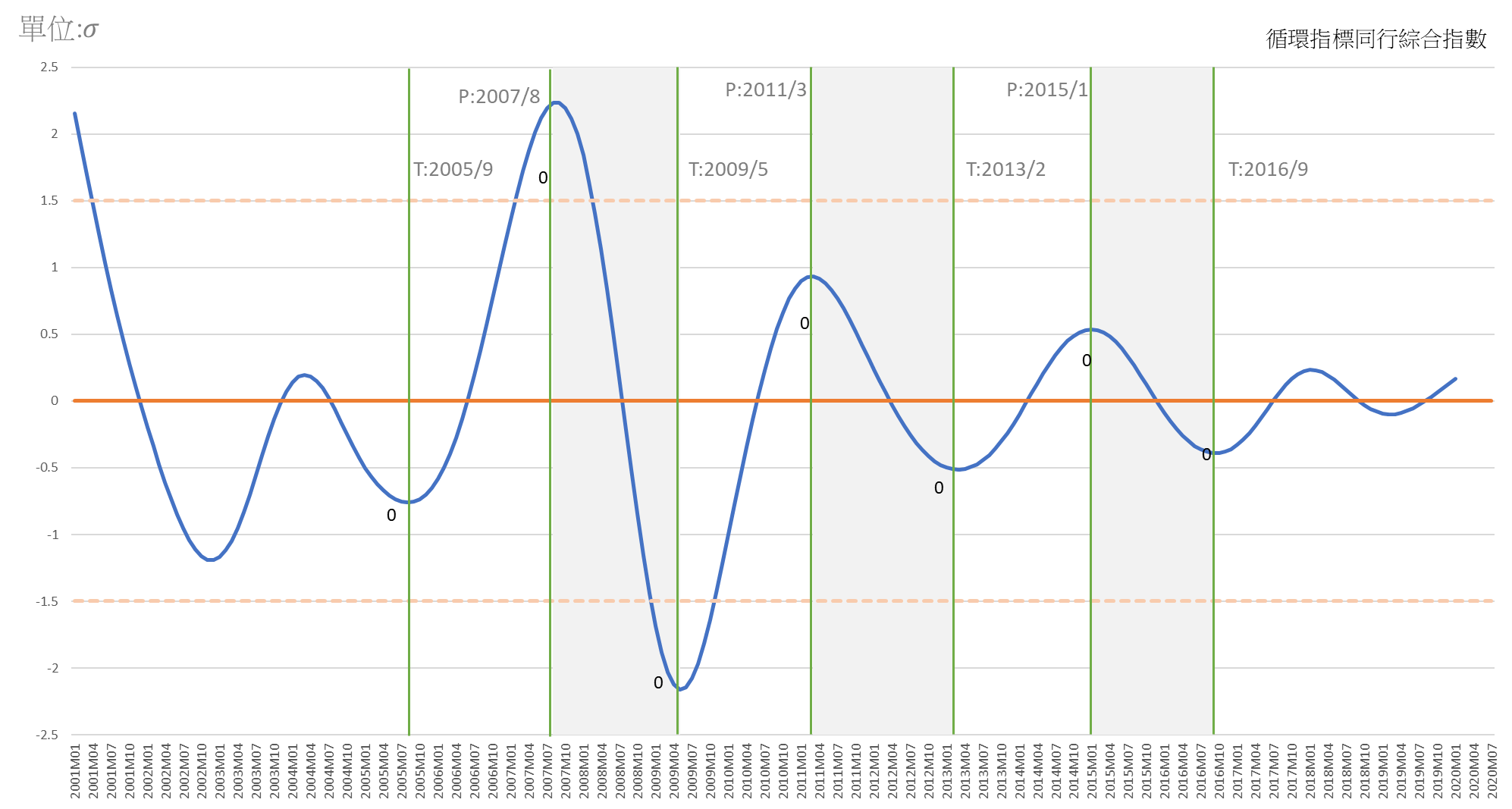

Commerce Development Research Institute(CDRI)released the Business Cycle Coincident Composite Index for Taiwan Service Industry today (5th March), prompted by the government's announcement that GDP in Q4 2019 rose by 3.3%, booming is expected all the way to July. The physical investment and financial activities continued to strengthen, effect to the employment sector. Leading indicators of unemployment benefits were initially recognized (inverted) but rose to a higher level, and the net entry rate of employees in the business services industry increased even more.

The structural overturn of coincident indicators is extremely obvious. The cyclical trend of the five major sub-indicators of the coincident indicators has all turned down in Q4 2019.

The following chart 1 shows the forecast of the business cycle index system. The Cyclical Coincident Composite Index for Service Industries, which represents the business cycle of the service industry, has been rising all the way since March 2019 due to the substantial improvement in Q4 2019.

Chart 1 Trend and Forecast of the Business Cycle Coincident Composite Index

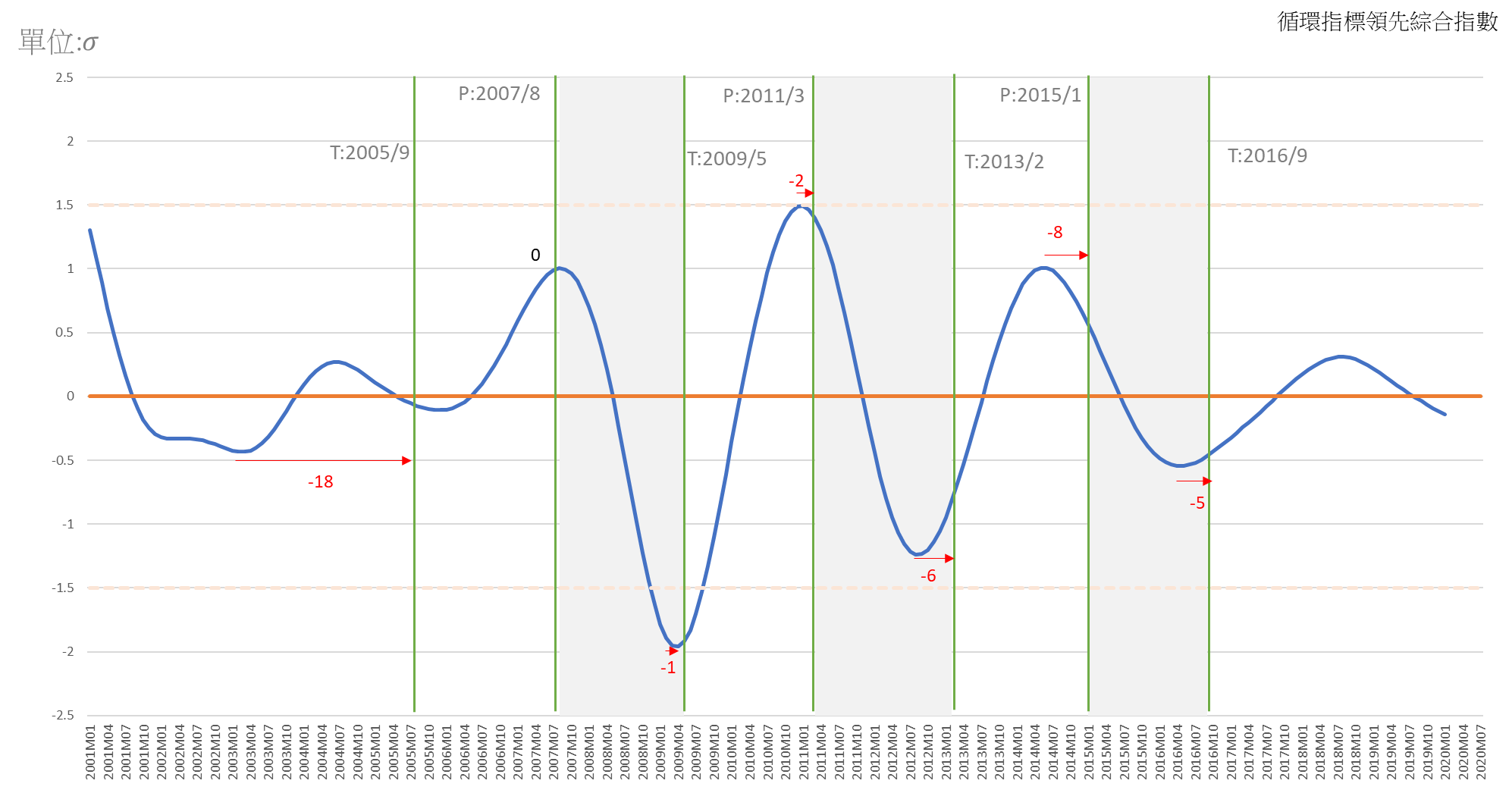

A. The actual value of Cyclical Leading Composite Index for Service Industries(Long-term trend excluded)peaked in August 2018, and then continued to decline until January. The real GDP of transportation and storage and the stock market continued to fall.

B. The overall result shows that the decline rate of the business cycle leading composite index of the service industry has slowed down significantly, but because of the widening gap between the sub-indicators of the data in Q4 last year, the differences of the composite cycle index has also increased.

1. Real GDP of Transportation and Storage

The GDP in Q4 kast year statistics showed a slight acceleration in the rate of decline. It is estimated that the cyclic index fell to 98.68 in January 2020, indicating that it is still difficult to see a rise-up in the short term.

2. Private Real Fixed Capital Formation

It has been continuously rising for 22 months, making the longest record of the expansion period of this indicator in the past 20 years. It was estimated that it could grow to 104.1 in January 2020.

3. The stock price index of the commercial service industry

It has continued to drop till January to 96.98, showing that the downward trend has continued to slow down slightly. In February, the epidemic began to impact the stock market as the world spread significantly but compared with the actual value of the stock price index in February and January, it only decreased by 1.26%, and there was no significant deterioration in the current downward trend.

4. Revenue and Expenditure of Service Trade

The international trade in services has a long-term deficit, but the deficit is affected by the business cycle and fluctuates relatively frequently. Before the structural factors of the global trade competitiveness of the service industry have not advanced fundamentally, the long-term trade deficit cannot be improved.

5. Initial recognition of unemployment benefits (reciprocal)

It has risen to 99.31 in January 2020, which should be related to the effect of the current investment. (Note that the short-term impact of the spread of the coronavirus epidemic on the service industry and employment is inevitable.)

6. Commercial service net employment rate

The estimate of 101.27 in January 2020 as in March 2015, showing progress in the difficulty.

C. After the analysis and forecast of the overall business cycle composite index of the commercial service industry, all five sub-indicators showed an upward trend. Although the increase in each sub-indicator is small, the overall index has an overturn.

1. Real GDP cyclical index of wholesale and retail

It has improved in Q4 2019, which is better than the previous period's estimation, in which the downward trend of the cyclic trend was slightly lower than the long-term trend, now it is rising higher than the long-term trend.

2. Real GDP of Finance and Insurance

The business cycle index started to rise in February 2019, and the cycle trend value has returned to 100.31 in December. It is estimated that it will continue to rise to 100.38 in January 2020, indicating that the economy is improving. This should be related to the return of Taiwanese people in business, digital economy, and 5G which brought investment funds and also the government's policy that has been supporting SMEs.

3. Real GDP of real estate and residential services

The latest analysis shows that the cyclic trend has continued to rise slightly over the past two years. The index had raised from 99.78 in June 2017 to 100.23 in December 2019. It is estimated to be 100.25 in January 2020. Yet there is still no apparent sign of improvement.

4. Residential services, utilities, and other fuel industries

The trend started to pick up from April 2019, with an index of 99.95. The cyclical index changed to 99.97 in December, and it is estimated to be 99.98 in January 2020 so far.

5. Number of employees in the service industry

The index began to fall in January 2018 and then fall below the long-term trend (100) in July 2018. It was 99.99 in November 2019 and the actual value 99.99 in December. It shows that the index fluctuates slightly up and down in the long-term trend, and not showing a growth of the business.

|

Year/Month

|

Cycle Indicators

(Unit: σ, Benchmark: 0)

|

Remark

|

|

2020-07

|

0.3329

|

(P)

|

Prediction based on the lead effect for six months of the ARMA Model:(4,0) (0,0)

|

|

2020-06

|

0.3141

|

(P)

|

|

2020-05

|

0.2912

|

(P)

|

|

2020-04

|

0.2646

|

(P)

|

|

2020-03

|

0.2350

|

(P)

|

|

2020-02

|

0.2030

|

(P)

|

|

2020-01

|

0.1695

|

(f)

|

The estimated value of the coincident composite index

|

|

2019-12

|

0.1351

|

(a)

|

The actual value of the coincident composite index

|

|

2019-11

|

0.1005

|

(a)

|

|

2019-10

|

0.0663

|

(a)

|

|

Source: Business Cycle Forecasting Team, CDRI

|

|

Note:

|

|

a

|

(actual)

|

|

|

|

f

|

(estimated)

|

|

|

|

p

|

(predicted)

|

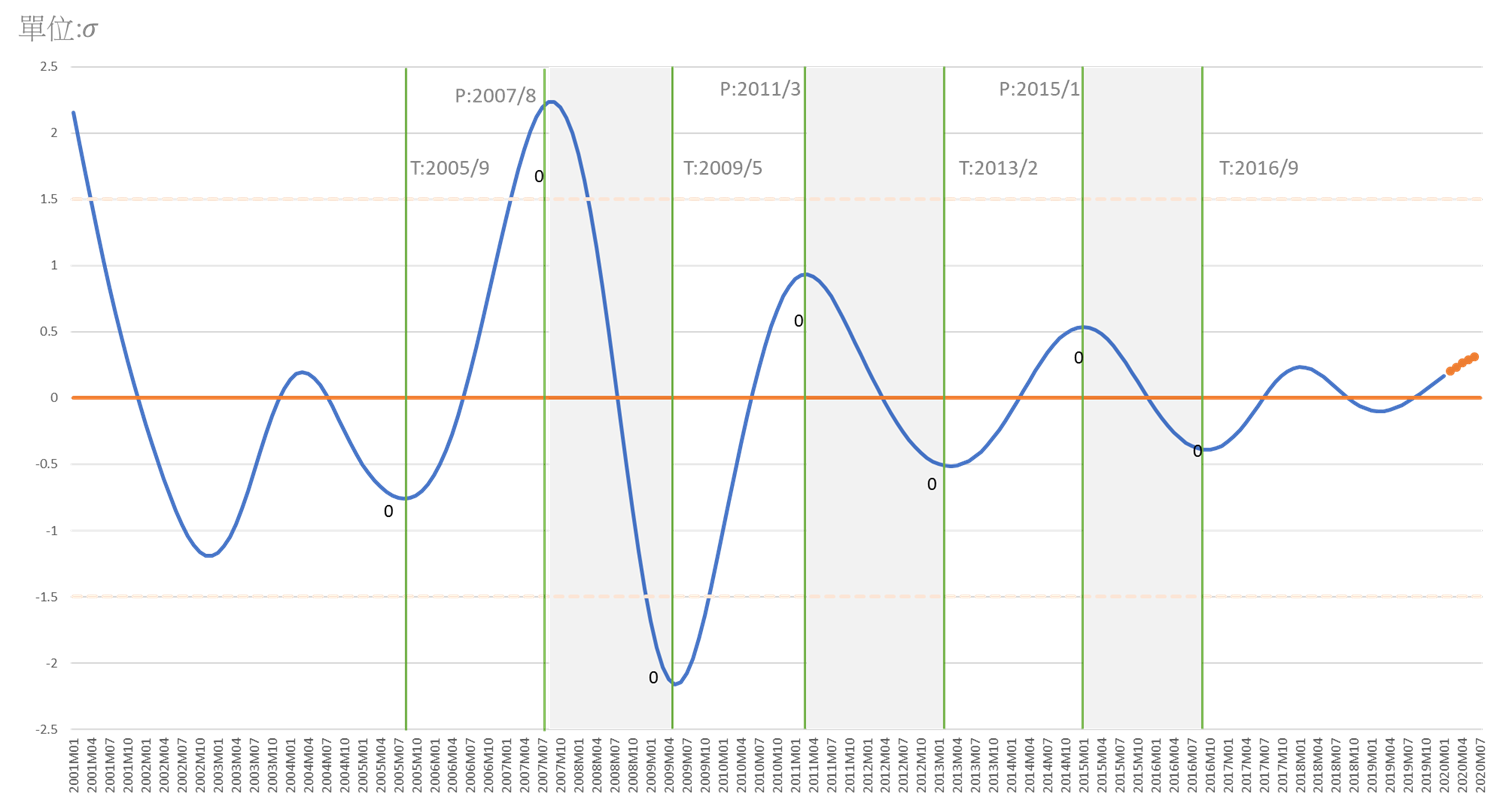

Business Cycle Coincident Composite Index for Taiwan Service Sector

Business Cycle Composite Index for Taiwan Service Sector

Source: Business Cycle Forecasting Team, CDRI

Previous Cycles:

|

Cycle

|

Trough

|

Peak

|

Trough

|

|

1

|

2005/9

|

2007/8

|

2009/5

|

|

2

|

2009/5

|

2011/3

|

2013/2

|

|

3

|

2013/2

|

2015/1

|

2016/9

|